Countries With the Lowest Taxes: Where is it More Advantageous for an Investor to Obtain Residence

The opportunity to optimise taxes is one of the reasons why investors obtain a residence permit or second citizenship. They choose countries that offer special tax regimes or fully exempt residents from paying certain taxes.

The conditions for using preferential tax regimes depend on the specific state and the resident’s status. In the article, we compare the jurisdictions of countries with investment programmes and examine where it is more advantageous to pay taxes.

What are preferential tax regimes and who are they available to?

A preferential tax regime is a special taxation system under which a state reduces or fully cancels certain taxes for investors and residents. The purpose of such measures is to attract capital to the country, create jobs, and strengthen the economy.

The state may not levy tax on income received abroad or may exempt investors from inheritance tax. In some countries, corporate tax rates are reduced so that it is more advantageous for businesses to register companies there.

A preferential regime does not mean full exemption from taxes. Domestic charges usually remain, such as VAT or property duties. Therefore, before choosing a tax jurisdiction, an investor needs to assess all conditions and compare them with their personal goals.

Preferential tax regimes are not universal. Access to them depends on a person’s status and the legislation of a specific country.

Tax residents

Most often, a preferential regime applies to those who have obtained tax resident status. It is determined by the time spent in the country. Usually, a person needs to live there for more than 183 days a year. To do this, foreigners obtain a residence permit, for example, by investment.

Some states introduce additional conditions for recognising a foreigner as a tax resident: having permanent housing, a centre of vital interests, or economic ties with the country. For example, in Cyprus, it is enough to spend 60 days a year there, but a person must also have housing and not be a tax resident of another country.

Citizens

Sometimes, tax concessions apply to all citizens of the country. For example, residents of Monaco or Andorra do not pay income tax. However, in most countries, a passport itself does not grant the right to tax benefits if a person lives abroad.

Foreign investors

Some states provide benefits to investors without requiring them to live in the country. This is how Caribbean citizenship by investment programmes work: a person obtains citizenship and an exemption from taxes on foreign income, even if they have never been to the country.

What benefits and deductions do countries with residence permits and citizenship by investment offer?

Countries with Golden Visa and

Tax holidays

Tax holidays are a full exemption from income tax for a specific period, usually

In 2026, Türkiye introduced a longer

Exemption from tax on foreign income

The

Depending on the country’s rules,

Fixed tax amount

A new tax resident pays an annual amount established by law instead of a percentage of foreign income. For example, in Italy, qualifying new residents may pay a flat substitute tax of €300,000 a year on

If a person’s income amounts to millions, a fixed tax rate is more advantageous than the standard progressive scale.

Capital gains benefits

In some countries, the sale of foreign assets is not taxed. An investor can sell shares or real estate abroad and not pay tax in the country of residence.

No inheritance and gift tax

Sometimes, one family member can transfer a business, bank accounts, or real estate to another, and children can inherit financial assets. In such cases, tax is usually levied.

Some countries exempt individuals from paying gift or inheritance tax. This opportunity is important for investors who think in advance about preserving capital for future generations.

Preferential tax regimes in Greece

Investors can get Golden Visas when they buy real estate or securities in Greece, invest in a business, or open a bank deposit. The investment amount starts at €250,000, and obtaining the status takes at least 4 months.

Tax benefits for individuals

The

Foreigners who have met one of 3 conditions have the right to claim the benefits:

- They became new taxpayers in Greece and had not been taxpayers there for 7 of the previous 8 years.

- They invested at least €500,000 in the country’s economy within the last 3 years before changing their tax residence.

- They obtained a Greek Golden Visa.

A 50% discount on income tax is paid by

To use the discount, a foreigner submits an application to the tax service and confirms that they work for a local company or have become an entrepreneur in Greece.

Benefits for pensioners. Foreign pensioners can transfer their tax residence to Greece and pay a flat tax of 7% on all foreign income for 15 years. The rate applies to all income from abroad: pensions, dividends, interest, income from renting out real estate, or income from the sale of assets.

The benefit is granted to those who have not been tax residents of Greece for the last 5 out of 6 years. A pensioner submits documents to the tax service and confirms the status of a foreign pension recipient [5] Source: Tax regime for foreign pensioners, Law 4714/2020, Article 5B .

Tax benefits for legal entities

Tax deduction for research and development, or R&D. Companies can deduct more from their taxable base than they actually spent on research, up to 315% of the amount of expenses. Each €1 of research expenses gives a company the right to reduce the base by €2,

Expenses for personnel, equipment, laboratory rent, materials, and intellectual property can be deducted if they are directly related to research. To apply the regime, companies submit a report to the tax service confirming that the business meets the R&D criteria.

Companies with international registration receive a profit tax exemption if they have income from the use of patents. The benefit applies for 3 years. If a company has invested money in R&D related to the patent, it receives an additional benefit, a 10% tax reduction for another 7 years [7] Source: Tax benefits for income, Law 5162/2024 .

Profit tax is also not levied on companies that are in the process of merger or division. At the same time, the right to depreciation, loss carryforward, and reserves is preserved

[8]

Source: Regulate tax neutrality in mergers, Law 4172/2013, Articles

Exemption from tax on dividends and capital gains from the sale of shares in subsidiaries. The benefit applies to companies with share capital, such as LLCs or

To use the benefits, 3 conditions must be met:

- Subsidiary pays corporate tax in its country.

- Company is not registered in a “

non-cooperative jurisdiction”. - Investor owns at least 10% of the shares and holds them for at least 24 months.

Tonnage tax is a special tax for shipowners in Greece. It replaces the 22% corporate tax and applies to all income from operating a vessel: transportation, leasing, dividends, and profit from the sale of the vessel.

The tax is calculated not on profit, but on the gross register tonnage of the vessel, or GRT. First, the The tax is calculated not on profit, but on the gross register tonnage of the vessel, or GRT. First, the tonnage is divided into ranges, and coefficients are applied:

- Up to 10,000 GRT — 1.2.

- 10,001 to 20,000 — 1.1.

- 20,001 to 40,000 — 1.0.

- 40,001 to 80,000 — 0.45.

- Over 80,000 — 0.2.

The result is multiplied by a rate that depends on the age of the vessel: from $0,407 per tonne for new vessels to $0,73 per tonne for old vessels. When the tax is paid, it is converted into euros at the Bank of Greece exchange rate on the payment date.

How to become a tax resident of Greece

Foreigners become tax residents if they spend more than 183 days a year in Greece and obtain an AFM tax number. The count starts from the date of crossing the border. The rule does not apply to tourists and people who come for medical treatment.

All tax residents over 18 years old are required to declare income, even income that is not taxed.

If a company is registered in Greece, it is automatically considered a tax resident and is required to pay corporate tax on all profits.

Preferential tax regimes in Portugal

The Portugal Golden Visa, or a residence permit by investment, is obtained by foreigners who invest in the country’s economy:

- at least €250,000 in the reconstruction of national heritage sites or support for cultural activities;

- €500,000 in the purchase of investment fund units, a local business, or scientific projects;

- open a company and create at least 10 jobs in Portugal.

Investors are only required to live in the country for 7 days a year. However, should they choose to relocate to Portugal and obtain tax residence there, several benefits are available.

Tax benefits for individuals

The IFICI regime is available to foreigners who have not been tax residents of Portugal for the last 5 years. Employment and

Benefits for repatriates. Portugal has launched a programme that reduces the tax burden for citizens returning from abroad. For 5 years after returning, they pay tax only on half of their employment or

To use the benefit, it is necessary to prove that the person:

- was already a tax resident of Portugal but has not been one for the last 5 years;

- has no debts to the country’s tax authorities;

- has not applied for

Non-Habitual Resident status [11] Source: Support programme, Programa Regressar .

There is no inheritance or gift tax for close relatives, spouses, children, and parents. If the property is received by a distant relative or an unrelated person, stamp duty of 10% applies.

Tax benefits for legal entities

Regional rate reductions. The main corporate tax rate in mainland Portugal is 19%. In the Autonomous Regions of Madeira and the Azores, the standard corporate tax rate is 13% for companies resident there and for permanent establishments registered in the regions.

Entities whose main activity is not commercial, industrial, or agricultural are taxed at 13.3% in Madeira and the Azores.

Benefits for startups and small businesses. For startups, the first €50,000 of profit is taxed at a rate of 12.5% instead of 19%. In Madeira, the rate is lower — 8.75%

[12]

Source: Regional IRC rate, Decree of the Legislative Assembly of Madeira No. 26/2022/M

. The same rates apply to companies operating in priority

For small and

Benefits for the Madeira special economic zone. Companies licensed within the Madeira International Business Centre can pay corporate tax at a reduced rate of 5% on taxable income. New entities can be incorporated under the current regime until December 31st, 2026, and the reduced rate applies until December 31st, 2033 [13] Source: Reduced corporate tax rate, Law No. 64/2015 of July 1st .

To use the regime, a company must:

- obtain a licence to operate from the Madeira administration;

- have a real presence: an office, employees, and expenses in the region;

- create jobs.

The benefit applies only to part of the

How to become a tax resident of Portugal

Tax residence is assigned to those who spend at least 183 days a year in the country or have their main place of residence in Portugal. To do this, one needs to have a tax number, NIF, and submit tax returns to local offices of the tax service, Serviço de Finanças.

All companies registered in Portugal are automatically recognised as tax residents and are required to pay corporate tax under the general rules.

Preferential tax regimes in Hungary

To obtain a residence permit in Hungary, investors choose one of two options: investments in local real estate funds of at least €250,000 or a donation to a higher education institution of at least €1,000,000. The process takes at least 5 months, and the status is issued immediately for 10 years.

Tax benefits for individuals

The country has a simplified KATA regime. It is suitable for

A fixed amount is paid every month — HUF 50,000, or €127. The payment covers all tax obligations: income tax, pension contributions, and social contributions.

The income limit is HUF 18 million a year, or €46,000. Revenue above this amount is taxed at a rate of 40%.

Tax benefits for legal entities

A company pays tax at a rate of 10% on the KIVA tax base, not on revenue. The tax base is generally calculated from

From 2026, KIVA is available to companies with fewer than 100 employees and annual revenue or balance sheet total of up to HUF 6 billion. Companies can remain under the regime until they reach 200 employees or HUF 12 billion in annual revenue or balance sheet total.

Both new and operating companies can choose this tax regime if they meet the conditions [15] Source: KIVA regime, Act No. 147 of 2012 .

To switch to the new tax regime, an application is submitted to the National Tax and Customs Administration. If it is approved, the company starts operating under the regime from the first day of the following month.

How to become a tax resident of Hungary

A foreigner becomes a tax resident if they spend at least 183 days a year in Hungary or have a centre of vital interests in the country: property, family, or a main business. To confirm residence, one needs to have a tax number and submit tax returns to the Hungarian tax authority, NAV.

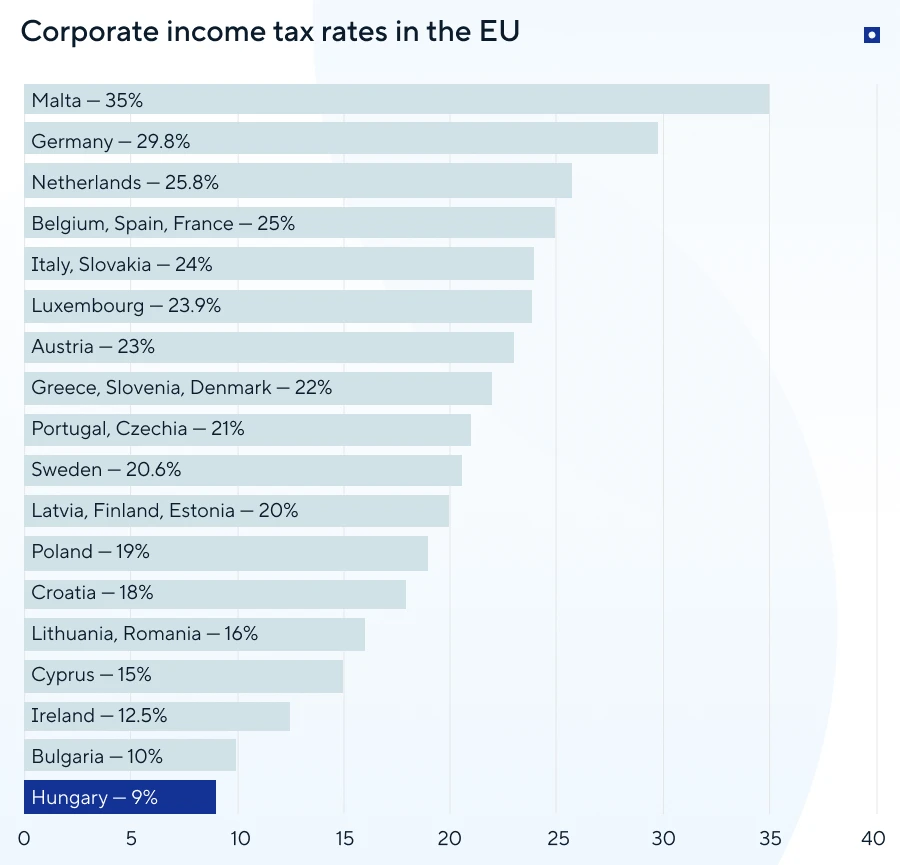

If a company is registered or effectively managed in Hungary, it is recognised as a tax resident and pays corporate income tax at a flat rate of 9% on its taxable profit.

Additional charges may also apply, including local business tax of up to 2% depending on the municipality and innovation contribution of 0.3% for companies that are not micro or small enterprises. Employers also pay social contribution tax of 13% on employees’ gross salaries.

Preferential tax regimes in Malta

In Malta, investors get a residence permit under the Malta Global Residence Programme. Applicants rent or buy real estate in the country and pay an administrative fee.

The investor becomes a tax resident of the country and pays tax on worldwide income remitted to Malta at a reduced rate of 15% instead of 35%. The minimum tax amount per year is €15,000 per family.

Tax benefits for individuals

Tax regime for foreign investors. They can choose one of the following options:

- rent a property in Malta for at least €9,600 a year;

- buy a property in Malta worth at least €275,000;

- rent a property in Gozo or the south of Malta for at least €8,750 a year;

- buy a property in Gozo or the south of Malta worth at least €220,000.

Applicants also pay an administrative fee and apply for special tax status under the Malta Global Residence Programme.

A special tax regime applies to residence permit holders by investment:

- 0% on income received abroad and not remitted to Malta;

- 15% on income received abroad and remitted to Malta;

- 35% on income received in Malta.

The minimum tax amount per year is €15,000 per family.

Tax regime for highly qualified workers. A flat personal income tax rate of 15% applies to employment income of specialists in finance, gaming, aviation, and assisted reproductive technology. To obtain the status, an applicant must have an employment contract for an eligible position with a company licensed or recognised by the competent Maltese authority

[16]

Source: Highly Qualified Persons Rules, Malta tax guidelines

. For the 2026 basis year, the minimum annual income must exceed €102,422. The benefit applies for 5 consecutive years for EEA and Swiss nationals and 4 consecutive years for

Malta Retirement Programme for pensioners. Foreigners pay personal income tax at a rate of 15% instead of the progressive scale from 0 to 35% if they remit their pension to Malta and spend it in the country.

To participate in the programme, one needs to buy or rent real estate and not work for local companies. The minimum tax under this programme is €7,500 a year for the main applicant and €500 for each dependant [17] Source: Tax rate for foreign pensioners, Malta Retirement Programme Rules .

No inheritance and gift tax. If property is transferred to children or a spouse, only stamp duty needs to be paid, from 2 to 5% of the value of the real estate or shares.

Tax benefits for legal entities

Malta Tax Refund System for shareholders. The corporate income tax rate in Malta is 35%. This is one of the highest rates in the European Union, but most of the amount paid can be returned through tax deductions:

- refund of 6/7 of the tax for trading and service

companies—an effective rate of around 5%; - refund of 5/7 for companies with passive interest or royalty

income—an effective rate of around 10%; - refund of 2/3 for companies that have already used a foreign tax

credit—an effective rate of up to 15% [18] Source: Refund of part of the tax to shareholders, Income Tax Act .

IP Box regime. Income from the use of patents, copyright, and other forms of intellectual property is taxed at a reduced rate of up to 10%, depending on the company’s cost structure [19] Source: Deductions on income from intellectual property, Patent Box Regime Rules .

Tonnage tax. If companies register vessels under the Maltese flag, they can choose to pay tax not on profit, but at fixed rates. The rate depends on the gross tonnage of the vessel and its age.

How to become a tax resident of Malta

Malta distinguishes between two types of tax residence: domiciled and

Domicile is a permanent place of residence that affects taxation. Domiciled residents pay tax on all worldwide income, regardless of the country where it is received.

Maltese citizens receive domicile at birth. Foreigners can obtain it if they are over 18 years old, have confirmed their intention to live on the island, for example by buying a house, and do not permanently live in another country.

All companies registered in Malta are considered tax residents and pay corporate tax at a rate of 35% before benefits and deductions are applied.

Preferential tax regimes in Cyprus

Investors obtain permanent residence in Cyprus if they invest at least €300,000 in real estate or securities in the country.

Tax benefits for individuals

Foreigners may partially avoid paying salary tax if they become tax residents of Cyprus for the first time.

If an employee’s annual income exceeds €55,000, 50% of their salary is exempt from income tax. The benefit applies for up to 17 years [20] Source: Income tax for employees, Cyprus Tax Department Circular 4/2024 .

If the salary is between €19,500 and 55,000, 20% of the amount is exempt from tax, but no more than €8,550 a year. This benefit applies for 7 years.

Tax benefits for legal entities

The special IP Box tax regime allows IT companies and owners of intellectual property to reduce tax on qualifying income from patents, copyrighted software, and other eligible assets. Under the regime, 80% of qualifying IP profits may be exempt from corporate tax.

As Cyprus increased its standard corporate tax rate from 12.5% to 15% in 2026, the effective tax rate under the IP Box regime is now about 3% instead of 2.5% [21] Source: Cyprus tax reform, KPMG .

Tonnage tax. Shipping companies and vessel owners can pay tax not on profit, but at fixed rates depending on the tonnage of the vessel. This exempts them from corporate tax and capital gains tax.

How to become a tax resident of Cyprus

A person is considered a tax resident if they spend more than 183 days in Cyprus during a year. All days spent on the island are counted. Days of entry and exit are counted as full days.

One can also become a tax resident of Cyprus after 60 days of living in the country. To do this, they must meet all 5 conditions:

- Not be a tax resident of another country.

- Not spend more than 183 days a year in another state.

- Live in Cyprus for at least 60 days a year.

- Have a permanent place of residence in the country, whether renting or buying housing.

- Conduct business, work as an employee, or hold a management position in a company that is a tax resident of the country.

There are two types of tax residence in Cyprus: domiciled and

A domiciled tax resident is a person who was born in Cyprus or has lived there for more than 17 of the last 20 years. They pay taxes on worldwide income, including special defence contributions. They are charged on dividends, interest, and rental income.

A

Companies registered in Cyprus are recognised as tax residents and pay corporate tax at a rate of 15%. From 2026, interest income earned by companies is also subject to corporate tax at 15% and is exempt from Special Defence Contribution.

Rental income is no longer subject to Special Defence Contribution and is taxed under the corporate income tax rules.

Preferential tax regimes in Italy

The Investor Visa for Italy allows foreigners to obtain a

Tax benefits for individuals

Flat tax regime for new residents.

The regime can apply for up to 15 years and may be extended to family members. In this case, an additional substitute tax of €50,000 a year is due for each family member covered by the option.

Benefits for repatriate workers. The regime was created to attract highly qualified specialists to Italy and encourage Italians living abroad to return.

Under the new regime, qualifying employees and

A more favourable rule applies to workers who move to Italy with a minor child or have a minor child after relocation. In this case, only 40% of qualifying income is taxable, which means that 60% of the income is exempt [22] Source: Tax regime for repatriate specialists, Legislative Decree No. 209/2023 .

To use the regime, a worker must transfer tax residence to Italy, meet the prior foreign residence requirement, work mainly in Italy, and remain tax resident in Italy for at least 4 years.

Tax benefits for legal entities

Patent Box is a special regime for companies that invest in intellectual property. It applies to research and development costs related to qualifying intangible assets, including copyrighted software, industrial patents, designs, and models.

Companies in Italy pay corporate tax, IRES, at a rate of 24% and regional tax, IRAP, generally at 3.9%. Under the current Patent Box regime, qualifying R&D costs can be increased by 110% for tax deduction purposes. This reduces the taxable base for IRES and IRAP.

For example, if a company incurs €1 million in qualifying R&D costs related to patented technology or copyrighted software, it may deduct an additional €1.1 million from its taxable base under the Patent Box regime [23] Source: Patent Box regime, Legislative Decree No.209/2023 .

Tonnage tax. For shipping companies, Italy applies a tonnage tax system: instead of corporate tax, they pay a fixed amount depending on the gross tonnage of vessels.

How to become a tax resident of Italy

A person is considered a tax resident of Italy if they meet at least one of the conditions for more than 183 days a year:

- Registered with a local municipality as a resident.

- Have a centre of vital interests in the country — housing, family, or main business.

- Actually live in Italy.

Companies are recognised as tax residents and pay taxes if they are registered in Italy.

Preferential tax regimes in Andorra

Foreigners apply for a residence permit in Andorra if they can meet the investment and financial requirements. In 2026, the standard investment threshold for passive residence increased to €1,000,000 in eligible Andorran assets.

A lower €400,000 route remains available through a contribution to the Housing Fund. Applicants also need to confirm sufficient income, usually at least 300% of the Andorran annual minimum wage. In 2026, this is around €54,900 for the main applicant.

Andorra has no special tax regimes for individuals. Personal income tax is charged at a general rate of 10%, but relief applies to lower income:

- income up to €24,000 is not taxed;

- income between €24,000 and €40,000 is effectively taxed at 5%;

- income over €40,000 is taxed at 10%.

In most European Union countries, the rates are significantly higher. For comparison, in neighbouring Portugal, the maximum personal income tax rate reaches 48%. In Germany, it is 45%.

Andorra residents also do not pay wealth and inheritance taxes.

Tax benefits for legal entities

Preferential regime for innovative companies. If companies operate in research, software development, biotechnology, or digital services, they can use a deduction regime. Up to 80% of income from the use or transfer of intellectual property rights is excluded from the taxable base.

Thanks to deductions, the corporate tax rate is reduced from 10% to

Preferential regime for holding companies. Income from owning foreign subsidiaries is exempt from taxation provided that the subsidiary pays tax in its country and is not registered in an offshore jurisdiction.

No withholding tax on dividends. In Andorra, companies do not withhold tax on dividends they pay to their shareholders. This rule applies to both residents and foreign investors.

How to become a tax resident of Andorra

To become a tax resident, one needs to live in the country for more than 183 days a year or have a centre of vital interests there, such as family or work.

All companies registered in the country are recognised as tax residents and are required to pay corporate tax at a rate of 10%.

Preferential tax regimes in the UAE

Foreigners can obtain a UAE Golden Visa if they invest in the country, buy real estate, or meet other eligibility criteria. In Dubai, real estate investors can apply for a

The UAE does not offer citizenship by investment, but it is one of the most popular

Tax benefits for individuals

The UAE does not levy personal income tax at the federal or emirate level [25] Source: Taxation, Official Portal of the UAE Government . This means that individuals do not pay personal income tax on salaries, dividends, interest, capital gains, and personal investment income.

The benefit is not a temporary tax holiday. It applies generally to individuals who live in the UAE, including foreign residents, Golden Visa holders, investors, and entrepreneurs.

However, moving to the UAE does not automatically cancel tax obligations in another country. Investors need to check whether they remain tax residents in their previous jurisdiction and whether their country of origin taxes worldwide income.

Tax benefits for legal entities

The UAE applies corporate tax to companies and other business entities. For most businesses, the rate is 0% on taxable income up to AED 375,000 and 9% on taxable income above this threshold.

Companies registered in UAE free zones may benefit from a 0% corporate tax rate on qualifying income. To use the benefit, a company must:

- Meet the conditions for a Qualifying Free Zone Person.

- Maintain adequate substance in the UAE.

- Comply with corporate tax reporting rules.

Income that does not meet the qualifying income criteria is taxed at the standard 9% rate. Therefore, investors who open a company in a UAE free zone need to assess the type of income, counterparties, substance requirements, and reporting obligations before choosing the structure.

What taxes remain in the UAE

The country applies 5% VAT to most goods and services. Excise tax applies to certain goods that are harmful to health, such as tobacco products and energy drinks.

Businesses may also pay corporate tax, customs duties, licence fees, municipal charges, and real

How to become a tax resident of the UAE

A person can be recognised as a UAE tax resident if one of the statutory criteria is met:

- Spending at least 183 days in the UAE during a consecutive

12-month period. - Spending at least 90 days in the UAE during a consecutive

12-month period and holding a UAE residence permit or having a permanent place of residence in the country. - Proving that the UAE is the person’s usual or primary place of residence and the centre of their financial and personal interests.

UAE tax residents can apply for a Tax Residency Certificate from the Federal Tax Authority. The certificate can be used to confirm tax residence and, where applicable, claim benefits under double tax treaties.

Tax benefits for investors in countries with Golden Visas: comparing conditions

Countries with Golden Visas offer different tax benefits for new residents. In some countries, a fixed tax is introduced instead of a progressive scale, while in others, the rate is reduced for specialists, or foreign income is exempt from tax.

Where to obtain a residence permit by investment and reduce the tax burden

| Country and investment threshold | How to become a tax resident | Tax benefits |

|---|---|---|

| Greece — €250,000+ | Live in the country for at least 183 days a year | 1. Fixed tax of €100,000 on worldwide income. 2. 50% discount on income tax for new employees and digital nomads. 3. Reduced tax of 7% on foreign income for pensioners. |

| Portugal — €250,000+ | Live in the country for at least 183 days a year or have a habitual residence there | 1. Reduced income tax of 20% for specialists working in science, technology, education, and innovation. 2. Tax on half of employment or 3. No inheritance or gift tax for close relatives. |

| Hungary — €250,000+ | Live in the country for at least 183 days a year or have a centre of vital interests there | Simplified tax regimes may apply: KATA for certain |

| Malta — €30,000+ | Special tax status under the Malta Global Residence Programme is available to applicants who hold residential property in Malta | 15% tax on income: • foreign income remitted to Malta by GRP beneficiaries; • foreign pension income remitted to Malta under the Malta Retirement Programme; • qualifying employment income of highly qualified specialists. |

| Cyprus — €300,000+ | Live in the country for at least 183 days a year. Another option is to live in Cyprus for at least 60 days a year, rent or buy housing, and work or run a business. | 1. For 17 years, 50% of employment income is exempt if the annual salary exceeds €55,000. 2. For 7 years, 20% of employment income may be exempt, capped at €8,550 a year. 3. |

| Italy — €250,000+ | For more than 183 days a year, meet one of three conditions: register as a resident, have a centre of vital interests, or actually live in the country. | 1. Fixed tax of €300,000 a year on 2. Foreign workers usually pay tax on 50% of qualifying income, up to €600,000 a year, for 5 tax years. 3. Pensioners may pay 7% tax on foreign income if they move to qualifying municipalities. |

| Andorra — €400,000+ | Live in the country for at least 183 days a year or have a centre of vital interests there | 1. No inheritance or wealth taxes. 2. Benefits for innovative companies: corporate tax rate may be reduced to 3. Benefits for holding companies: income from qualifying foreign subsidiaries may be exempt. 4. Dividends are not subject to withholding tax. |

| UAE — $545,000 | Live in the country for at least 183 days a year or live in the UAE for at least 90 days a year, hold a residence permit, and have a home, employment, or business there | 1. No personal income tax on individuals. 2. Corporate tax is 0% on taxable income up to AED 375,000 and 9% on taxable income above this threshold. 3. Free zone companies may benefit from 0% corporate tax on qualifying income. |

Preferential tax regimes in countries that grant citizenship by investment

Vanuatu citizenship by investment starts with a

The country does not have many taxes that are common in other countries: individuals do not pay personal income tax, corporate income tax, wealth tax, capital gains tax, or tax on worldwide income.

Legal entities are exempt from paying tax during the first 20 years of a company’s operation. Instead, they pay an annual fee of $300.

Under Sierra Leone’s

Sierra Leone has no special tax regimes. Benefits apply in specific sectors: for mining and oil companies, the rate is reduced to 25%; for manufacturing enterprises outside the capital, it is reduced to 15%.

Türkiye citizenship by investment requires a minimum investment of $400,000 in real estate, or $500,000 under other qualifying routes, such as a bank deposit, government bonds, investment fund units, or fixed capital investment.

Türkiye introduced a

- Move to Türkiye and become a Turkish tax resident.

- Provided they had neither a domicile nor tax liability in Türkiye during the 3 calendar years before relocation.

The exemption covers only income received outside Türkiye. This may include:

- foreign dividends;

- business income;

- investment income;

- income from assets abroad.

Such income is not included in the annual Turkish tax return. If the resident files a return for other reasons, exempt foreign income is still not declared.

Income from sources in Türkiye remains taxable. Depending on the amount of income, the personal income tax rate ranges from 15 to 40%.

The same law also introduced a reduced inheritance and gift tax rate of 1% for residents who use the

Caribbean countries. St Kitts and Nevis, Dominica, Antigua and Barbuda, Grenada, and St Lucia do not tax capital gains, inheritance, and gifts. This simplifies asset transfer and the management of international income.

St Kitts and Nevis, as well as Antigua and Barbuda, do not have personal income tax or tax on worldwide income. In the other three Caribbean countries, basic progressive personal and corporate income tax rates apply, and there are no special regimes.

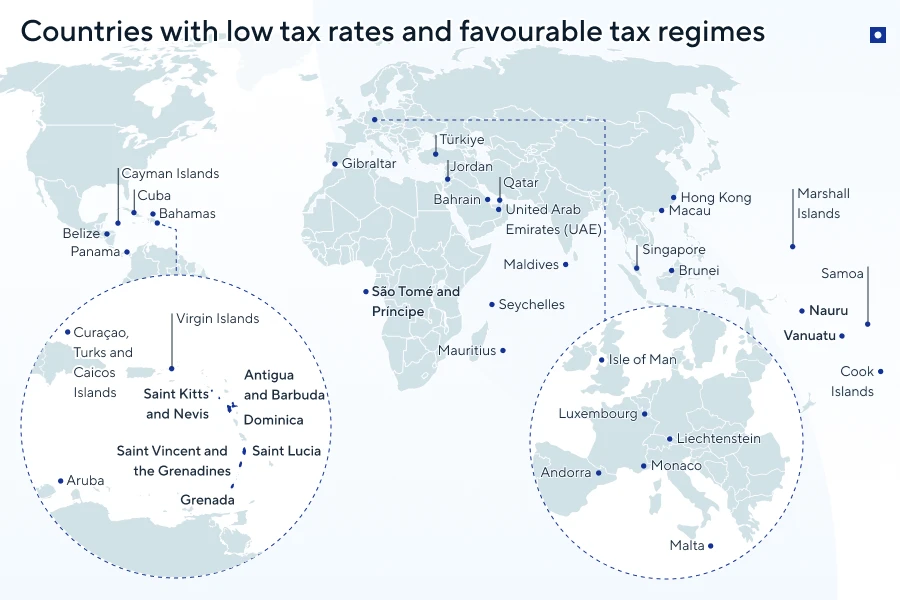

Other countries with preferential tax regimes

Some countries are less often associated with investment migration but still attract investors and wealthy individuals with low or zero personal taxes.

Monaco is one of the most established

The Bahamas, the Cayman Islands, and Bermuda are also known for low personal taxation. They usually fund their budgets through VAT, customs duties, stamp duties, business licence fees, tourism charges, and financial services.

Bahrain, Kuwait, Qatar, Saudi Arabia, and Oman are often chosen by entrepreneurs, executives, and business owners who want access to the Gulf market and developed infrastructure.

These jurisdictions can be useful for relocation, asset planning, or business structuring. However, a low tax rate is not enough to choose a country. Investors also need to assess residence rules, reporting obligations, banking requirements, cost of living, and tax obligations in their previous country of residence.

Key points about tax regimes and benefits

- A preferential tax regime reduces or cancels taxes for investors and residents. States offer benefits to attract capital, create jobs, and strengthen the economy.

- To become a tax resident, in most countries one needs to live on their territory for at least 183 days a year or have a centre of vital interests there.

- Usually, countries with residence permits by investment offer special tax conditions for wealthy foreigners: fixed income tax rates, benefits on foreign income, or exemption from inheritance tax.

- Cyprus and Malta apply the

Non-Dom regime. This means that tax is paid only on income within the country, while dividends and interest from abroad are exempt. - In a number of countries, corporate taxes are reduced in certain regions or for specific business sectors, such as innovation, shipping, or startups.

About the authors

Frequently asked questions

Benefits for new tax residents are available in many countries. For example, Portugal used to have the NHR regime, but in 2024 it was replaced by the IFICI regime, which reduces taxes for specialists in science, technology, and innovation.

In Italy, wealthy foreigners pay a fixed tax of €300,000 on worldwide income under the

Spain has the Beckham Law, which allows foreign specialists to pay a fixed rate of 24% on income received in Spain.

Under the territorial principle, tax is charged only on income within the country. For example, in Malta, residents without domicile pay tax only on income remitted to the country.

When worldwide income is taxed, tax is levied on all income.

It depends on the chosen jurisdiction. In Greece, investors under the

Golden Visa holders are required to maintain the investment for the entire validity period of the status. Selling the asset, such as real estate or securities, automatically leads to the loss of the residence permit.

An exception applies when the investor has already obtained citizenship. For example, real estate in Greece can be sold after obtaining citizenship following 7 years of residence in the country.

The Common Reporting Standard, or CRS, is an international standard for the automatic exchange of tax information. It requires banks to transfer account data to the country of tax residence. Therefore, when tax residence changes, the information becomes available to the tax service of another country.

If an investor obtains a Golden Visa and becomes a tax resident, they are required to declare income in the new jurisdiction. For example, in Cyprus, all tax residents over 18 years old must submit tax returns, even if their income is not taxed.

Caribbean countries and Vanuatu exempt tax residents from tax on dividends, capital gains, and inheritance. This makes them attractive for investors who manage capital around the world.

Exit tax applies in Germany, France, the Netherlands, Canada, Israel, and the USA. In these countries, when tax residence changes, the state records capital gains and charges tax.

Owners of foreign real estate pay an annual property ownership tax, purchase fees, tax on rental income, capital gains tax on sale, and tax or fees on inheritance and gifts. The set of payments depends on the country, region, property value, type of real estate, and the owner’s tax status.

Countries with the lowest real estate taxes are the UAE, Vanuatu, Monaco, the Cayman Islands, and the Turks and Caicos Islands.

Read also

Contact us today

Passportivity assists international clients in obtaining residence and citizenship under the respective programs. Contact us to arrange an initial private consultation.